The increase in the volume of non-tourism services is one of the main surprises that the Spanish economy has witnessed in recent years, due to the severity of the phenomenon and its unintended nature. These services include a combination of professional activities, consulting, technology, research, logistics, finance and various administrative tasks. It is thus a very heterogeneous group of branches, although it is mainly aimed at companies. The difference between construction, agriculture, tourism and industry, mainly intended for homes, while public services have the mission of bringing value to society in general.

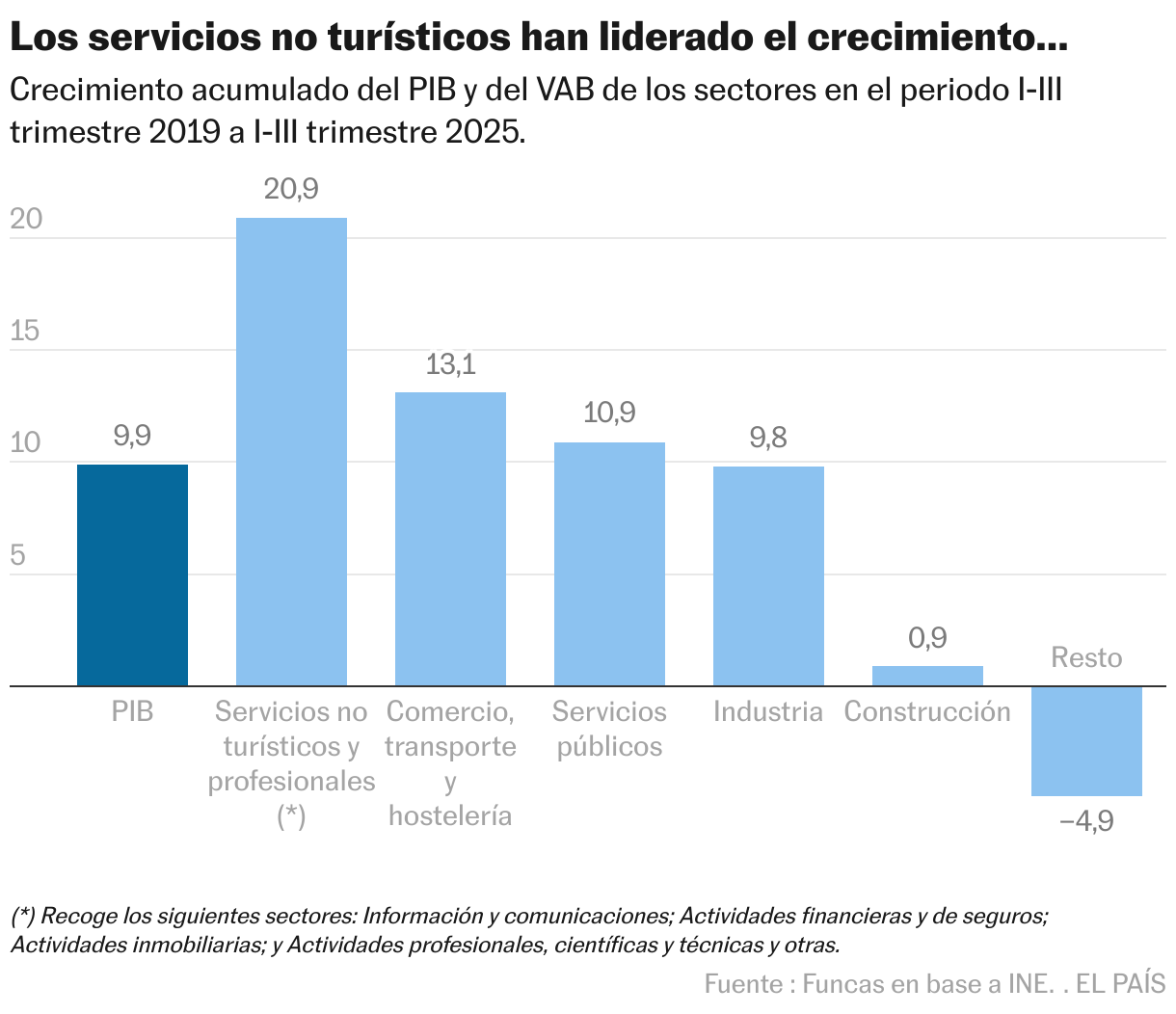

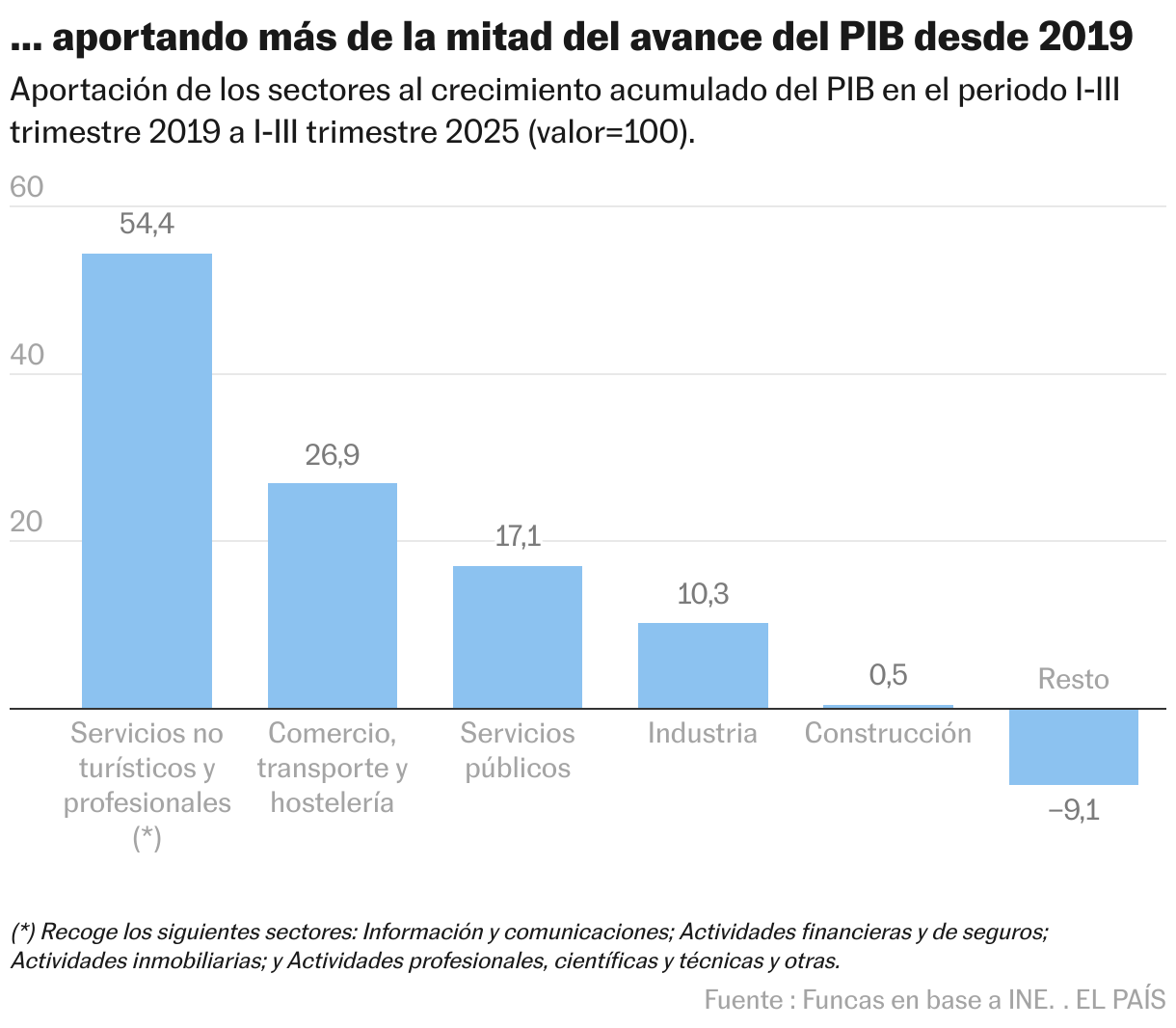

Economic policy has prioritized industrial development, enjoying the crown of European financing and, more recently, construction. However, it is these non-tourist services that have contributed most to the good moment for the economy. The wealth, and value added, generated by these services has increased by a staggering 21% in total in the latest glossary, more than double the group of productive sectors (data for the first three quarters of 2025 compared to the same period in 2019). These services explain more than a small portion of the GDP growth recorded in this period.

Its expansion reveals a structural change that began after the outbreak of the real estate crisis and accelerated after the pandemic. In 2007, construction represented 12% of GDP, and today it has reached the minimum. The lost ground was occupied (albeit entirely) by non-tourism services, whose contribution to the balance of payments was also notable: today the balance between exports and imports, which was negligible decades ago, is about 2.5% of GDP, which is close to the sacred tourism surplus.

The surpluses gained by non-tourism services have withstood all the crises that have occurred recently, in contrast to tourism, which was punished by the pandemic, and industry, the sector most vulnerable to the rise of airlines and the geopolitical tensions affecting the planet.

All of this serves to reinforce the current expansionary cycle and provides useful economic policy advice. First, the peak of non-tourism services has not been translated into a production model. In other words, these sectors remain the same engines of growth as the Spanish economy as a whole, relying heavily on the integration of the labor force as a support for activity, while productivity is characterized by its weakness.

In the case of services, this growth agenda faces a more serious sustainability problem than sectors such as construction or tourism, which could continue to expand by resorting to migration. On the other hand, professional or technological activities have to compete for scarce talent at the global level and retain young people who feel drawn to other destinations that offer better working conditions.

On the other hand, non-tourism services are relatively investment-intensive in “intangible assets”, intangible assets such as digital platform connectivity, technological capital and computer applications. The difficulty of recognizing this type of assets as collateral for obtaining new financing constitutes an obstacle, which also affects companies’ growth and thus productivity. These ideas should inspire the expansion of remaining next-generation funds into horizontal measures that address barriers to investment and design expansion of promising projects.

In short, the economy diversified thanks to the strengthening of a strong non-tourism service sector, which contributed to strengthening the expansionary cycle. However, transforming it into a model capable of maintaining high levels of productivity and wages remains an outstanding task.

External balance

The balance of payments depends solely on the uncertainties surrounding the development of international trade. The current account balance resulted in a surplus of €37,900 million as of September, 8.5% lower than in the same period last year. The sharp deterioration of the imbalance in international exchanges – as a result of the stagnation of the European market and, to a lesser extent, the increase in exports – was compensated by the surplus in the balance of services, tourism and non-tourism. Likewise, foreign direct investment fell less than expected.