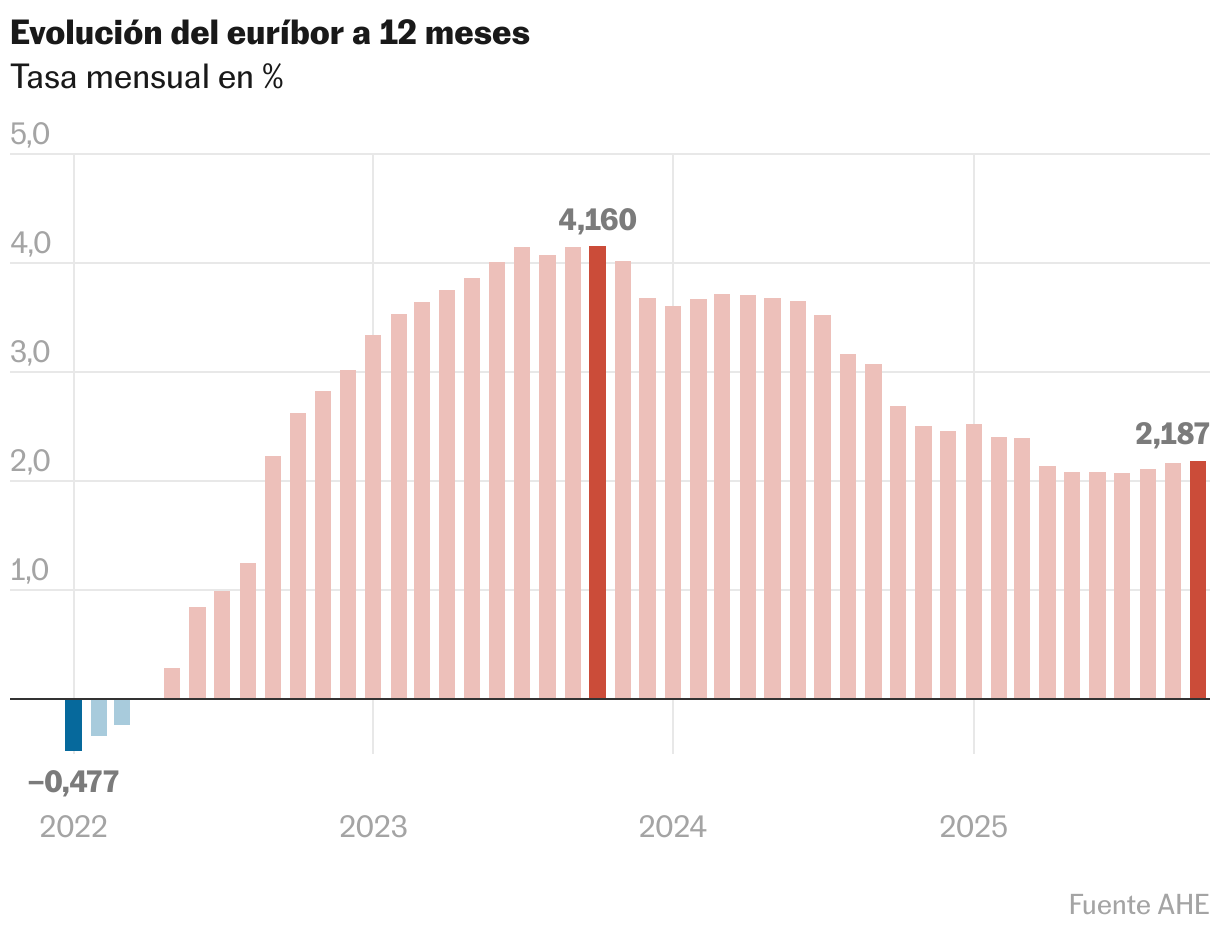

Looking at your checking account can bring unexpected moments of relief. More than one mortgage holder has found themselves in recent months with reductions in the installments they paid for their home loan. Many still benefit from these cuts, which leave more money in citizens’ pockets and less in banks’ budgets. However, the trend suggests that opening a financial institution order may become less fun in the future: EuroBor closed November at 2.217%, marking its fourth consecutive rise.

This number is the worst since last March. However, the euro faces an uncertain final stretch for the year, given that there is no sign that the ECB will return it to the path of declines seen in 2024 and the first half of 2025. With inflation under control – it is at a comfortable level of 2.1% in the eurozone – and with expectations that prices will not suffer major fluctuations in the medium term, Frankfurt is keeping interest rates frozen, estimating that the current level of 2% is the right type, the so-called neutral type, Which neither stimulates activity nor slows it down.

This paralysis has been negative for the Euribor, as a few months ago the ECB was expected to make at least one additional interest rate cut – the most optimistic of which was a cut of up to 1.5% – before adopting a policy of stagnation. This is causing a bit of a downturn: in October mortgages with a semi-annual review became more expensive for the first time in nearly two years.

For those with an annual review, this negative milestone will likely be delayed until spring, as long as there is no sudden change in trend. Meanwhile, in November of this year, the average mortgage, which in Spain, according to the National Institute of Statistics, amounts to 145,673 euros repaid over 25 years, will still save about 32 euros per month, or in other words, 385 euros per year.

Mortgages are more expensive

According to mortgage comparison company HelpMyCash, the rise in Euribor has already been transferred to the interest bill for those seeking to buy a home via a loan application. “Entities no longer expect further interest rate cuts, so they have no incentive to reduce their mortgage offerings. Some have begun to increase interest rates to gain some margin, especially those with a large market share,” he warns.

According to their data, at least seven banks increased interest on mortgage loans compared to mid-summer: Banco Santander, BBVA, Bankinter, COINC, Cajasiete, Unicaja and ING. “The largest increases have occurred in fixed mortgages for these entities,” they add.

Currently, this has not translated into a reduction in operations. In September, 46,120 mortgages were signed, the highest number during the entire year, and an increase of 12% compared to the same month last year, according to data published by the National Institute of Statistics (INE) on Thursday. If we take this year’s cumulative total, 367,715 mortgages were signed, 64,852 more than in the first nine months of 2024. All this despite the fact that prices continue without interruption: the average amount granted per mortgage in September was 171,612 euros, 14.1% more than last year.

The positive reading is that during these four months of Eurobor increases, the increase has not been very high, just two tenths of the lows in May, when it reached 2.024% in the daily rate, about to break the 2% barrier, so the financial hit to households has been limited. “The Euribor rate stabilizes in a narrow range, reducing monthly fluctuations and restoring predictability to households relying on a variable mortgage,” says Pablo Vega, expert at mortgage comparison company Rooms.