The ECB’s sudden shift in monetary policy during the recent inflationary crisis not only made variable and hybrid mortgages more expensive, it also revived an old tax deduction that had been in steady decline in Spain for years. A rise in interest rates, triggered by a Frankfurt offensive to try to stem rising prices, in 2023 will lead to the first rise in more than 15 years in the financial cost associated with the rebate for purchasing a primary residence, a benefit the government abolished in 2013 and which has since remained in a transitional regime.

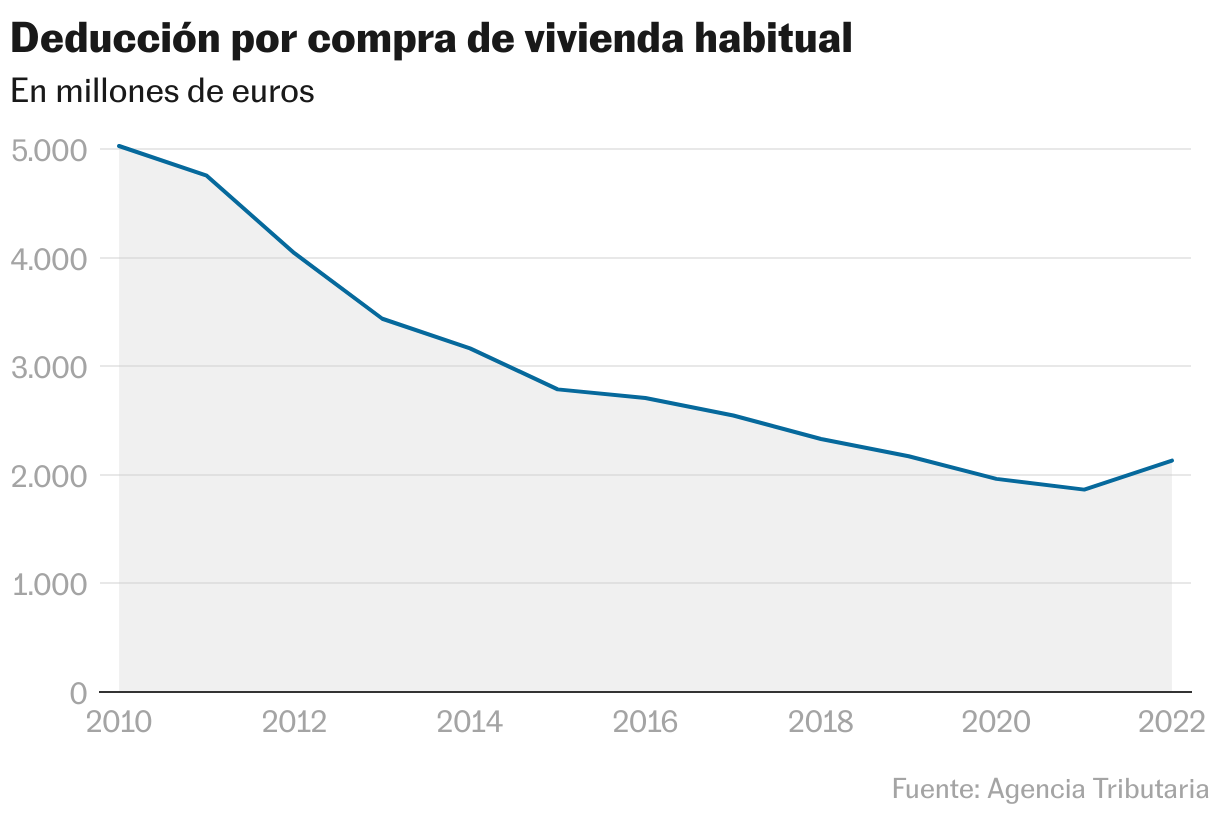

Official data collected by the tax agency clearly reflects the change in trend. After reaching the minimum in 2022, with a collection cost to the Ministry of Finance of 1,843 million euros, the total amount of deduction increased in 2023 to 2,268 million, an increase of 23%. It is an unexpected rise in a historical series that has witnessed nothing but decline since 2008.

The income tax deduction for investing in a primary residence has been, for a long time, one of the most popular tax benefits in Spain. Taxpayers are allowed to subtract 15% of the personal income tax rate from amounts paid each year to purchase or finance the main residence, up to a maximum of €9,040 per year. Although the deduction was abolished in 2013 in one of the amendment plans drawn up by CEO Mariano Rajoy, the legislator maintained a transitional system for those who obtained their habitual residence before that date.

The cancellation of the new procurement feature led to a gradual and continuous decline in impact: from the Treasury cost of 6,138 million in 2008, it moved little by little to 3,438 million in 2013, then to 2,170 million in 2019, and then to 1,843 million in 2022. The path was logical. With the door closed to new beneficiaries, the number of taxpayers eligible for the deduction decreased each year as they repaid their loan. Furthermore, as interest rates fall and the EURIBOR stabilizes, the amount of interest paid and hence the discount applied.

This trend was completely broken in 2023. Eurobors started the year rising strongly and ended it at about 4%, making new loans significantly more expensive and, at the same time, variable and hybrid mortgages that had already been signed for years. Average premiums for these credits became more expensive, and the increase automatically increased the deductible amounts in personal income tax for taxpayers who were still eligible for the benefit.

The more than 2.2 billion euros that the Treasury stopped collecting in 2023 due to withholding, as explained by José García Montalvo, professor of economics at the Pompeu Fabra University in Barcelona, is a number very similar to the figure recorded five years ago. However, at that time the Euribor rate was negative, while in 2023 it exceeded 4%.

Montalvo goes on to say that this effect of higher interest rates would have neutralized, to a large extent, the natural decline in the stock of mortgages with the right to deduct, which declines every year when loans reach their temporary limit or are paid off early. Furthermore, higher interest rates could have led to more early cancellations, also affecting mortgages that are still tax-deductible, although to a lesser extent depending on the remaining term of the loan.

The discount mechanisms remain the same as they were before their cancellation. Those who signed their mortgage before 1 January 2013 can deduct 15% of what was paid in the year (principal, interest and associated insurance), up to a maximum of €9,040 per year. The Treasury returns a maximum amount of €1,356 per taxpayer, or double if the return is filed individually by loan holders.

Despite this rebound in financial impact, the number of recipients continues to decline, and today is less than half what it was at the end of the real estate bubble, when about seven million applicants took the discount.

In recent months, the Central Administrative Economic Court, under the Ministry of the Treasury, has adopted a more flexible interpretation of the deduction, adjusting criteria that had until now been somewhat restricted by the tax agency. Among the most significant changes, the court recognized in April last year that taxpayers who acquired their housing before January 1, 2013 can apply the deduction to payments made in subsequent years, even if they did not claim it in previous years, as long as they were not required to file an income tax return due to insufficient income.

TEAC also recently clarified that canceling a mortgage loan along with the funds generated from the sale of the property can be considered a deductible investment, opening the door to potential returns. Until now, the Treasury has limited the deduction only to fees paid up to the day before the transfer.