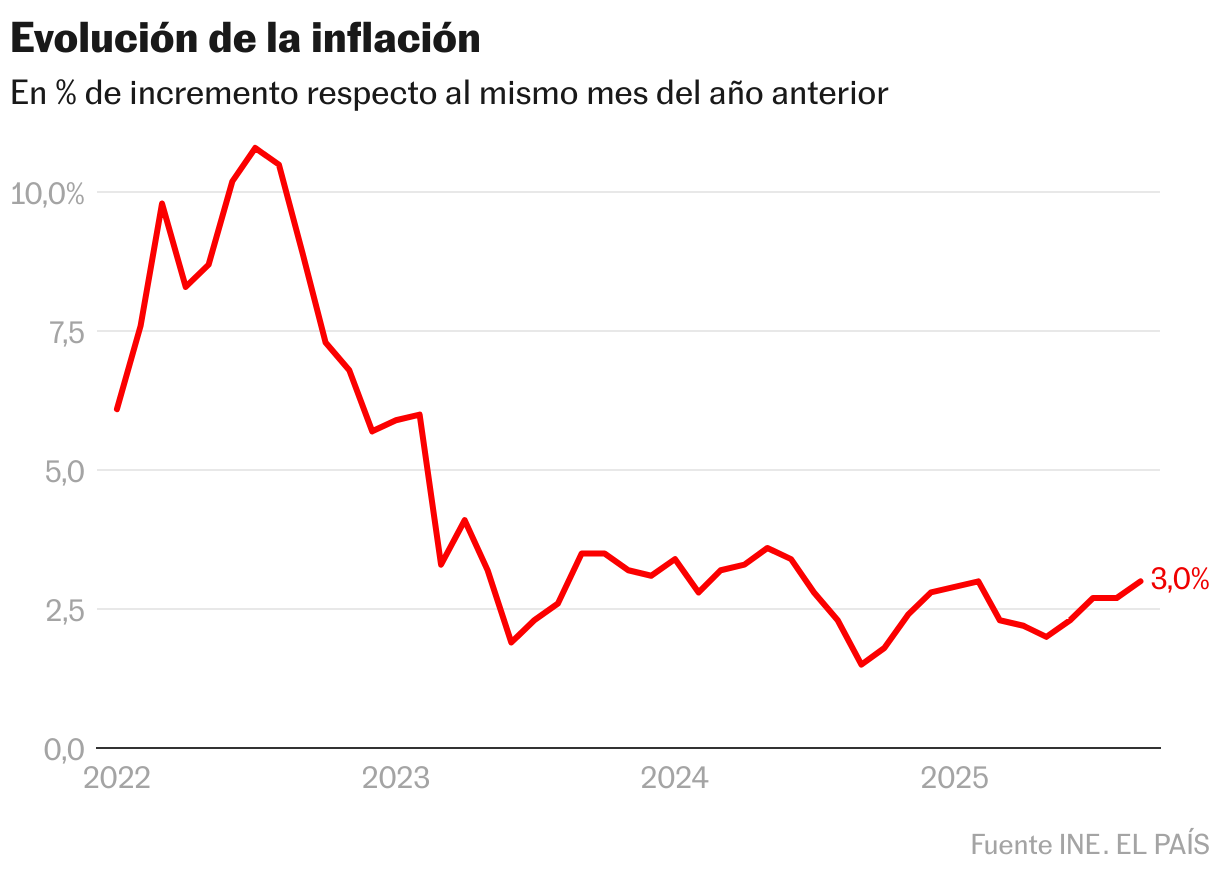

Spain ended the year with inflation at 2.9%, and it ends… at 2.9%. The circular movement of prices, which began the financial year where it began, according to the advanced data from December published this March by the National Institute of Statistics, was full of peaks, with a very favorable spring that unfolded over the months. This deterioration caused the annual average to fall to 2.7%, making it impossible to normalize prices to the objective levels of the European Central Bank (2%).

In the specific case of December, prices moderated by a tenth in November, thanks to the drop in fuel prices, but the gap with the euro zone remained almost intact, with a negative inflation differential around one point. A problem for the competitiveness of exporting companies.

It is clear that the average rate improved in 2024, when it was 2.8%, but very slightly. Electricity prices have significantly influenced the data, to the detriment, to the point that BBVA Research calculates that its price has increased by 8% since the blackout, and that there will be a tenth increase in GDP in 2025 and 2026. The paradox is that, despite the increase, the bank’s research department estimates that the price of electricity in the majority Spanish market remains more than 20% lower than what is paid in the rest of Europe.

CaixaBank Research agrees by giving capital importance to the behavior of the price of light. “The moderation of inflation in the coming months will largely depend on energy prices, particularly electricity. The international outlook for energy is favorable, even if at the national level there remains a certain uncertainty linked to electricity. On the one hand, in the field of energy, the PVPC (Voluntary Price of Small Consumers, the regulated tariff) will integrate into its calculation changes which should bring greater stability to the price of electricity. On the other On the other hand, the renegotiation of contracts on the open market could generate high prices.

The historic blackout that hit Spain in late April was a turning point, as it prompted authorities to take extra precautions and rely more on gas stations to prevent a repeat of the blackout. This sums up the disappearance of tax measures which reduced the energy bill, which would explain the increase in prices from year to year from the end of 2024 to the beginning of 2025.

For Ángel Talavera, chief economist for Europe at Oxford Economics, the gap with euro shareholders is normal, because it causes much stronger growth in the Spanish economy, which tends to warm up prices. However, it should be noted that the gap in contained inflation (with an average of 2.3% this year) is relatively small when compared to the differences in GDP rates, where Spain clearly dominates among the major economies. “The component that influences the most is electricity, which is supposed to be balanced. In other words, the gap implies a small loss of competitiveness, which if it persists for a long time, only becomes a problem”, he analyzes.

Core inflation, which excludes the prices of energy and unprocessed food products from its calculation, saw a more pronounced decline, of six tenths compared to the annual average of 2.9% for 2024, the date on which the government clings to defend that Spain is getting closer to the ECB’s target.

purchasing power

When will this fight with Europe end and can we achieve normalized inflation? BBVA Research estimates that this could still take some time, although rates will continue to moderate slowly, to 2.5% in 2026 and 2.2% in 2027, which will facilitate the recovery of the purchasing power of wages and support the recovery of private consumption. “This will be facilitated by the growth in labor income, which is increasing mainly thanks to the increase in job creation, but also thanks to the gradual rise in wages,” he underlined in his latest report. Spanish situation.

In this context, monetary policy will not be an ally. The European Central Bank is now prioritizing the stability of this type of interest, frozen at 2%, because the difference between what is happening in Spain and the Eurozone is that inflation is under control. Therefore, in the short term, increases are not expected that could contribute to moderating Spanish inflation.

This is already contributing to the de-escalation of the behavior of Brent oil (the benchmark in Europe), which is at annual lows of around $60 per barrel, and of the price of natural gas, which saw only a small percentage of its value last year and lost more than 90% of the peak following the invasion of Ukraine. It is also the strength of the euro against the dollar which reduces purchases abroad, particularly energy.

One of the most notable consequences of this increase in inflation in Spain will be seen in the increase in pensions, which will ultimately reach 2.7% next year. Indeed, for the calculation, the average inflation rate of the last months between the current year and the previous year is taken as a reference.