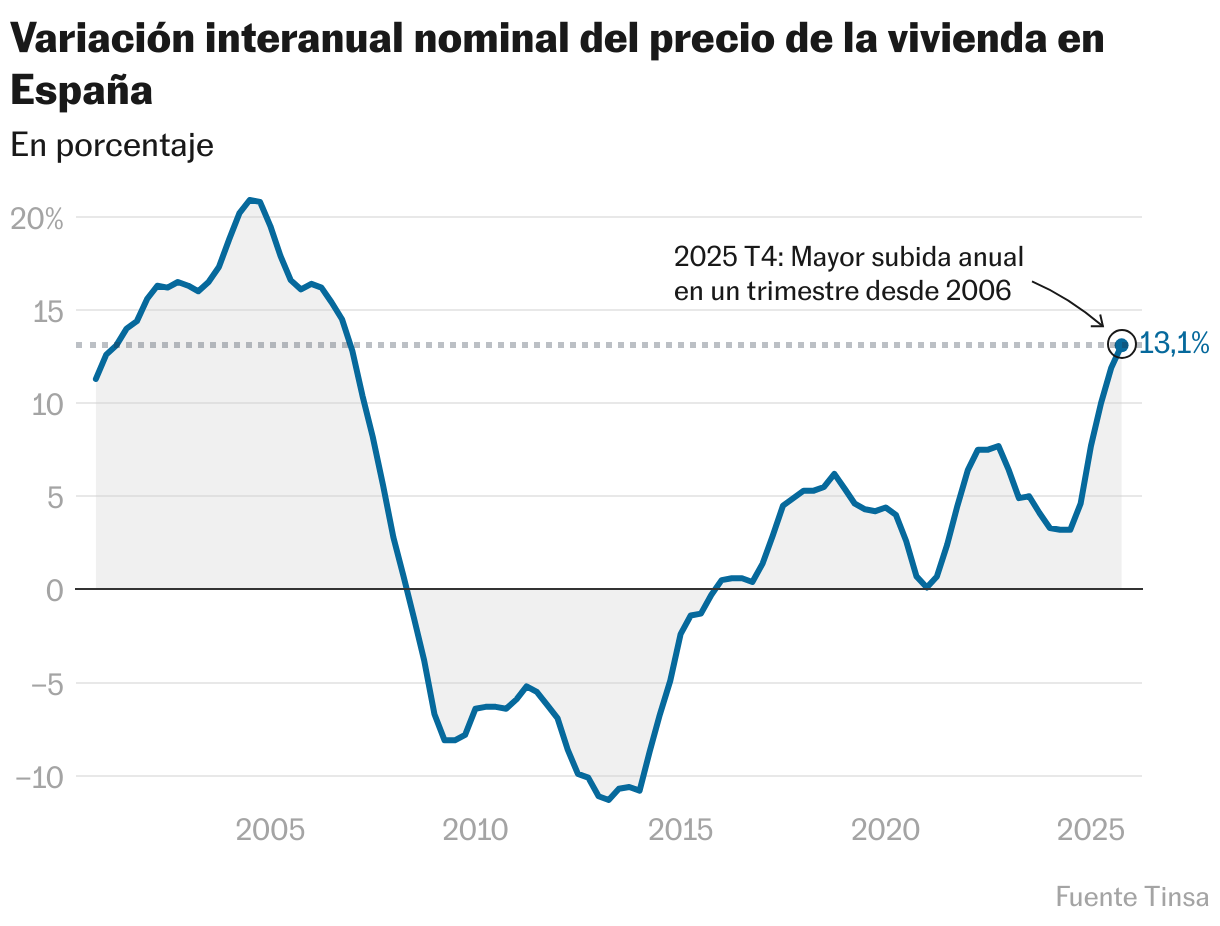

The Spanish residential market became very tense again in 2025, accelerating in the last part of the year a pace not seen since 2006. Far from moderating, real estate prices accelerated their growth and became more expensive by 13.1% year-on-year in the fourth quarter, an increase which, even without taking into account the effect of inflation, amounts to 10%, according to data published Monday by the expert Tinsa, the largest of the country. Both in nominal terms and after subtracting the CPI, these are the two largest annual quarterly increases in almost 20 years, before the bursting of the housing bubble.

After the pandemic, when the market stopped almost cold due to the health shutdown, real estate prices began to gradually increase. In nominal terms, they recorded increases of up to 7.7% in 2022. Subsequently, the pace moderated, with increases that were of the order of 4%. This trend suddenly reversed starting in the second quarter of this year, when increases began to exceed 10%.

Several factors combine to explain the prolonged rise in real estate prices: a labor market which showed notable resistance, the normalization of household purchasing power after the inflationary surge, the fall and then stabilization of mortgage costs after the rate cuts by the European Central Bank (ECB) in the first half of the year, the effect of real estate investment and the creation of new households. In short, supply incapable of absorbing demand.

The square meter reached on average 2,091 euros in the fourth quarter, only 3.3% less than the maximum reached in the fourth quarter of 2007, considered the peak of the bubble. Since the minimum recorded in the summer of 2015, the price in Spain has increased by almost 63.8%. Excluding the effect of inflation, the benchmark is 33% below the 2007 ceiling and 29% above the 2015 floor.

The increase in prices is generalized throughout the territory, although not homogeneous. Housing increased in all autonomous regions, but at different rates, with a range between 1.5% and 19.6%. In 11 territories, the price increase exceeds 10%. The highest intensities are concentrated in Madrid, which is leading the growth, followed by the Valencian Community and Cantabria (both close to 16%).

In nominal terms, the highest amounts are paid in Madrid (3,799 euros per square meter), the Balearic Islands (3,644 euros) and Catalonia (2,549 euros). At the opposite extreme are Castilla y León (1,274 euros per square meter), Castilla-La Mancha (1,164 euros) and Extremadura (976 euros).

The provincial analysis reinforces the idea that prices are accelerating. In 32 of the 52 provinces, price increases are intensifying and in 21 of them annual growth exceeds 10%, compared to only 13 in the previous quarter. The greatest tensions are in and around Madrid, on the Mediterranean coast, on the islands and in certain areas of the Cantabrian coast. At the same time, the evaluator confirms that the weakness is easing in traditionally lagging areas: Zamora, which recorded declines, is now moving towards stabilization.

All these dynamics are accentuated in the provincial capitals, which act as poles of attraction because they concentrate a large part of employment and offer the highest returns. In 20 of the 52 cases, year-on-year increases of more than 10% were recorded, compared to 15 in the third quarter, and the range of variation widened to be between 1.3% and the maximum of 20.9% recorded in Madrid. For its part, Barcelona accelerates to 8.3%. Alongside them, coastal capitals and archipelagos such as Valencia, Palma, Málaga, Alicante, Santander and Granada stand out, as well as certain inland cities which are intensifying their growth rate.

In fact, 10 of these cities already exceed the maximum prices of the 2007 peak in nominal terms, having added La Coruña, San Sebastián and Alicante to a group that already included Palma, Madrid, Málaga, Santa Cruz de Tenerife, Valencia, Pontevedra and Melilla. Excluding the CPI, they are all still lower, although Palma comes close.

This sustained increase in prices has a direct impact on housing accessibility. Nationally, the purchasing effort rate is around 34.5% of average household disposable income, a level that is still considered relatively reasonable – although it exceeds the 30% that the National Housing Act considers affordable housing conditions – thanks to improving purchasing power and moderating mortgage costs. This average, however, hides strong territorial imbalances. Five of the six major capitals exceed the critical threshold considered reasonable. Madrid requires a theoretical effort of 56%, Malaga 55%, Barcelona 53%, Seville 46% and Valencia 45%. Only Zaragoza remains at moderate levels, with 30%.

The trend for 2026 is the same. Cristina Arias, director of the Tinsa by Accumin research service, explains that next year the average price will continue to grow “between 5% and 10% in the current context of housing shortage, in line with a gradual stabilization of demand and the progressive incorporation, although still insufficient, of housing into the stock”.

New housing, as much as possible

The average price of new housing intensified its pace of growth at the end of December with an annual increase of 8.9% and a half-year increase of 4.7%, reaching a new historic maximum (3,298 euros per square meter), according to data also published this Monday by the Valuation Company.

By autonomy, Catalonia, Madrid and the Basque Country (respectively 5,288 euros, 5,172 euros and 3,582 euros per square meter) record the highest price of new housing in absolute figures. All three exceed the national average. Alongside them, six other communities are reaching peaks in terms of new construction: Andalusia, Asturias, the Balearic Islands, the Canary Islands, the Valencian Community and Galicia.

The expert’s forecasts suggest that the trend will continue in the coming months. Thus, at the end of the first quarter of 2026, an average price of 3,365 euros per square meter is projected, which would mean an interannual increase of 8.9% and a little lower, of 4.3%, semi-annually.